When it comes to financing, whether for personal needs, business growth, or major purchases, Canadians have a wide range of options to choose from. However, with so many choices available, finding the best deal can feel overwhelming. This guide will help you compare financing options in Canada, understand the pros and cons of each, and make an informed decision tailored to your needs.

Why Comparing Financing Options is Crucial

Before diving into the specifics, it’s important to understand why comparing financing options is essential. Not all loans or financing solutions are created equal. Interest rates, repayment terms, fees, and eligibility criteria can vary significantly between lenders. By comparing your options, you can:

- Save money on interest and fees

- Find flexible repayment terms

- Avoid hidden charges

- Choose a lender that aligns with your financial goals

Types of Financing Options in Canada

Canada offers a variety of financing options to suit different needs. Below, we’ll explore the most popular ones, including personal loans, business loans, mortgages, and lines of credit.

1. Personal Loans

Personal loans are one of the most common financing options in Canada. They can be used for a variety of purposes, such as debt consolidation, home renovations, or unexpected expenses.

Pros of Personal Loans

- Fixed interest rates for predictable payments

- No collateral required (for unsecured loans)

- Flexible repayment terms (usually 1–7 years)

Cons of Personal Loans

- Higher interest rates for unsecured loans

- Strict eligibility criteria (e.g., credit score, income)

- Potential for origination fees or prepayment penalties

Best For

- Individuals with good credit scores

- One-time expenses like weddings or medical bills

2. Business Loans

For entrepreneurs and small business owners, business loans are a lifeline for growth and operations. These loans can be used for equipment purchases, inventory, or expansion.

Pros of Business Loans

- Dedicated funding for business needs

- Competitive interest rates for established businesses

- Potential tax benefits on interest payments

Cons of Business Loans

- Requires a solid business plan and financial history

- Collateral may be required for larger loans

- Longer approval process compared to personal loans

Best For

- Small businesses looking to expand

- Startups with a clear revenue model

3. Mortgages

A mortgage is a long-term loan used to purchase real estate. With Canada’s competitive housing market, understanding your mortgage options is crucial.

Pros of Mortgages

- Low interest rates compared to other loan types

- Long repayment terms (up to 30 years)

- Build equity in your home over time

Cons of Mortgages

- Requires a significant down payment (usually 5%–20%)

- Strict eligibility criteria (e.g., income, credit score)

- Risk of foreclosure if payments are missed

Best For

- First-time homebuyers

- Real estate investors

4. Lines of Credit

A line of credit (LOC) is a flexible financing option that allows you to borrow up to a predetermined limit. You only pay interest on the amount you use.

Pros of Lines of Credit

- Flexible borrowing and repayment

- Lower interest rates compared to credit cards

- Reusable once repaid

Cons of Lines of Credit

- Variable interest rates can increase over time

- Requires discipline to avoid overspending

- May have annual fees

Best For

- Ongoing expenses like home renovations or education

- Emergency funds

5. Credit Cards

While not a traditional loan, credit cards are a form of revolving credit that can be used for everyday expenses or emergencies.

Pros of Credit Cards

- Convenient for small purchases

- Rewards programs (e.g., cashback, travel points)

- No collateral required

Cons of Credit Cards

- High interest rates if balances are not paid in full

- Can lead to debt accumulation

- Annual fees for premium cards

Best For

- Everyday expenses

- Building credit history

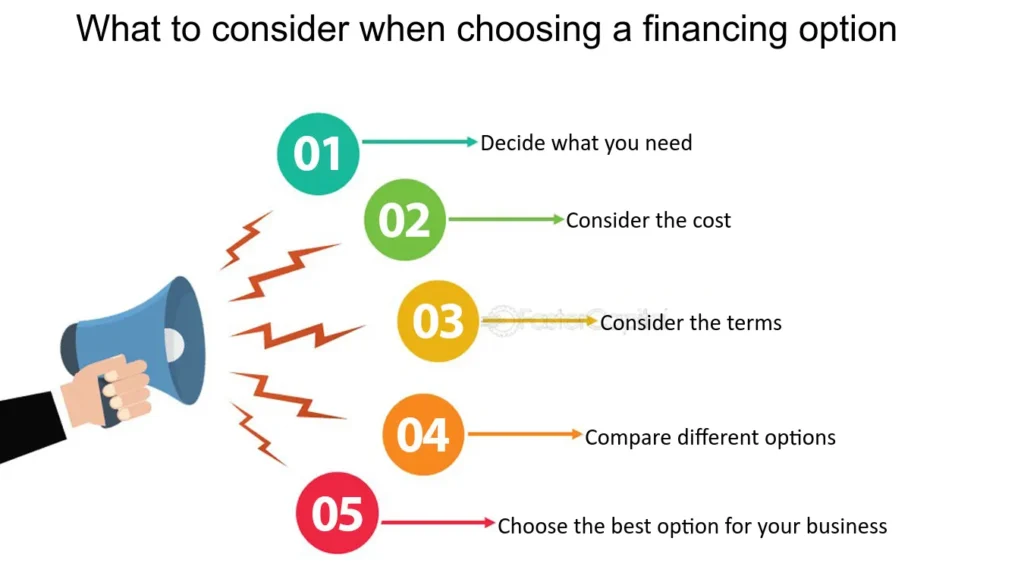

How to Compare Financing Options in Canada

Now that you know the types of financing available, here’s how to compare them effectively:

1. Interest Rates

Interest rates are one of the most important factors to consider. Even a small difference in rates can save you thousands of dollars over the life of a loan.

- Fixed vs. Variable Rates: Fixed rates remain the same throughout the loan term, while variable rates can fluctuate with market conditions.

- Annual Percentage Rate (APR): This includes both the interest rate and any additional fees, giving you a clearer picture of the total cost.

2. Repayment Terms

The length of your loan term affects both your monthly payments and the total interest paid.

- Shorter Terms: Higher monthly payments but lower overall interest.

- Longer Terms: Lower monthly payments but higher total interest.

3. Fees and Charges

Always read the fine print to understand any additional fees, such as:

- Origination fees

- Prepayment penalties

- Late payment fees

- Annual maintenance fees

4. Eligibility Criteria

Different lenders have different requirements. Common eligibility factors include:

- Credit score

- Income level

- Employment history

- Collateral (for secured loans)

5. Lender Reputation

Choose a reputable lender with positive customer reviews and transparent terms. Check for:

- Accreditation by regulatory bodies

- Customer service quality

- Online reviews and ratings

Top Lenders for Financing in Canada

Here are some of the top lenders in Canada to consider:

1. Banks

- RBC (Royal Bank of Canada): Offers a wide range of personal and business loans.

- TD Canada Trust: Known for competitive mortgage rates.

- Scotiabank: Great for lines of credit and international banking.

2. Credit Unions

- Vancity: Offers personalized service and competitive rates.

- Desjardins: Popular in Quebec for its community-focused approach.

3. Online Lenders

- Fairstone: Specializes in personal loans for borrowers with less-than-perfect credit.

- Lendful: Offers low-interest personal loans with fast approval.

Tips for Choosing the Best Financing Option

- Assess Your Needs: Determine how much you need to borrow and what you’ll use the funds for.

- Check Your Credit Score: A higher score can qualify you for better rates.

- Shop Around: Compare offers from multiple lenders to find the best deal.

- Read the Fine Print: Understand all terms and conditions before signing.

- Seek Professional Advice: Consult a financial advisor if you’re unsure.

Conclusion

Finding the best financing option in Canada requires careful research and comparison. Whether you’re looking for a personal loan, business loan, mortgage, or line of credit, understanding the pros and cons of each option will help you make an informed decision. By considering factors like interest rates, repayment terms, and lender reputation, you can secure a financing solution that meets your needs and supports your financial goals.

Remember, the right financing option is out there – you just need to find it!